Redefining Client Engagement Strategies for Financial Advisors in the Digital Age

Good news for financial advisors: According to Accenture field research, 52 percent of consumers are interested in upping their financial literacy. However, the downside to this trend is that they’re not necessarily taking traditional routes.

Consider the role that social media is playing. A full 56 percent of younger adults are willing to put their wealth management trust in influencers, per Credit Karma. Unfortunately, this practice is leading to some bad #FinTok ideas being disseminated. And that’s just one of the many hurdles that financial advisors need to clear in the digital age.

52 percent of consumers are interested in upping their financial literacy.

A full 56 percent of younger adults are willing to put their wealth management trust in influencers.

Another challenge facing financial advisors is the expectation that they provide more services to their offerings for nominal or no fees. After all, since people are getting advice for nothing online, they are reluctant to see value in paying for personal finance recommendations. At the same time, they want deeper relationships (again, for free) with the financial advisors they choose.

Essentially, what consumers want from their financial advisors is the same thing they’re asking for in brands: personalization. McKinsey and Company showed in 2021 that 71 percent of people want customized interactions with companies. That desire has spilled over into the financial landscape, necessitating that financial advisors do more, even if they have limited capacity. Despite this being a tall order, individualizing customer engagement is worth the effort.

71 percent of people want customized interactions with companies.

Advantages of Driving Personalization with Financial Clients

Financial advisors who put a premium on forging stronger ties with their clients will be more likely to edge out their competitors. Personalizing everything from communication to advice helps strengthen the bonds of trust. When clients feel heard, respected and understood, they’re more likely to see the relationship with their financial advisors as long-term.

A financial advisor who develops those types of meaningful connections with clients is more apt to enjoy higher client satisfaction ratings, too. With higher satisfaction comes the probability of increased future referrals. Consequently, even though tailoring financial advice and prioritizing regular interactions can be time-consuming, it can produce lucrative and measurable results.

With that being said, personalization can seem daunting at first. If you’re a financial advisor ready to break the mold, try the following techniques to ramp up your customization practices and deliver “Wow!” experiences to your clients.

1. Leverage technology.

Financial advisors today have tech tools to help them automate all aspects of their services. From scheduling appointments and sending out reminders to managing basic inquiries and social listening, they can free up their time for personal touchpoints. At the same time, they can collect data to improve and inform future communications, campaigns and initiatives.

Part of staying tech-forward is being present on social media and other digital platforms. It’s easier than ever to share pertinent content, market insights, client stories and more to foster connections with clients.

2. Stay on top of industry trends.

It’s the age of the robo-advisor, and human financial advisors shouldn’t look away. A better choice is to understand robo-advising and be able to provide complementary services to those who rely on robo-advisors’ AI algorithms to guide their investment and financial planning decisions and portfolio creation.

Remember: Robo-advisors have lowered conventional barriers to entry into wealth management. That’s hardly a bad thing because it allows more people to achieve financial goals. Many financial advisors have even started integrating robo-advising into their services mix. They’re leaning into the speed of robo-advisors and then helping clients tweak suggestions in a more personalized way.

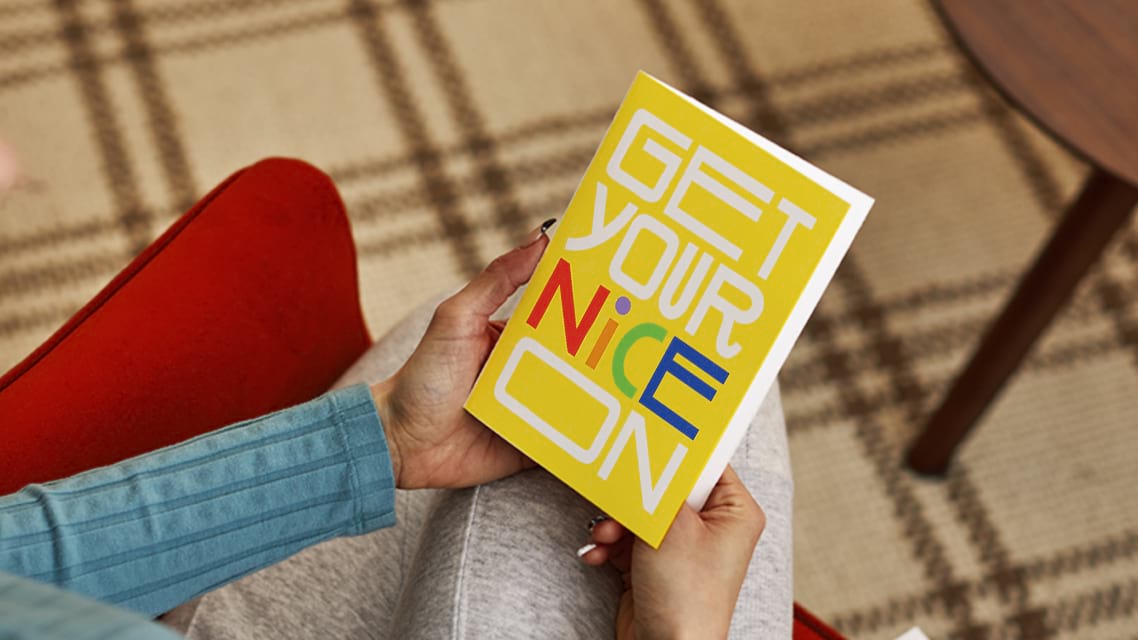

3. Go “old school” with handwritten notes.

Handwritten notes can make a positive impact in the digital age. For example, sending out special occasion cards and notes on holidays, birthdays or other client milestone dates can leave a lasting impression. A warm greeting card isn’t expected, which is why it feels fresh, welcoming and individualized.

Business greeting cards aren’t only received with appreciation by older consumers, either. Across the adult population, there's a notable preference for the personal touch of physical cards. Millennials are now leading in terms of dollars spent on greeting cards in the U.S., averaging $6 per card. More importantly, eight out of 10 people agree that greeting cards cannot be replaced by social media.

This trend highlights the enduring value of handwritten notes, especially for financial advisors. In an industry that is built on trust and personal connections, a greeting card can significantly enhance client relationships, conveying a level of personal attention and care that digital communication simply cannot match.

4. Educate leads and clients.

Despite the proliferation of financial talk online, financial literacy isn’t as high as it could be. Many people remain baffled about how to approach investing or financial planning. What they want is to learn more in an interactive, value-packed way.

Financial advisors can set up both in-person and online community events like workshops to attract prospects and educate clients. Events of this type strengthen relationships and highlight the advisor’s thought leadership and expertise. They also provide moments of conversation between attendees regarding their personal experiences. These interactions build community and reinforce the financial advisor's skill in helping and supporting people and families of varying situations.

5. Prioritize regular client communications.

Regular check-ins via phone calls, emails, texts, newsletters and in-person events help advisors stay top of mind with clients. The key to getting the most mileage out of these communications is ensuring they’re not just focused on cold or dry financial updates. On the contrary, they should include personalized content that aligns with the client’s interests or life situation.

Financial advisors can show their empathetic sides by routinely sending out information or content on topics that dovetail with the client’s experiences and realities. Empathy promotes better client relationships, which opens the door for long-lasting partnerships.

Financial advising has changed over the years, yet one thing remains the same: Clients want to feel that their unique needs are acknowledged and considered by their financial advisors. By implementing proactive strategies, advisors can achieve more for themselves and those they serve.

Jada Sudbeck is the sales and marketing director at Hallmark Business Connections. This wholly owned subsidiary of Hallmark Cards helps businesses strengthen relationships with their customers and employees by deepening emotional connections with them through life event marketing.

In this Article

Similar Articles